The Innovation Race: How China’s Polysilicon Industry Has Upped Its Game

Solar-grade polysilicon mass-production started in the early 2000s when the German government ramped up the promotion of clean energy.

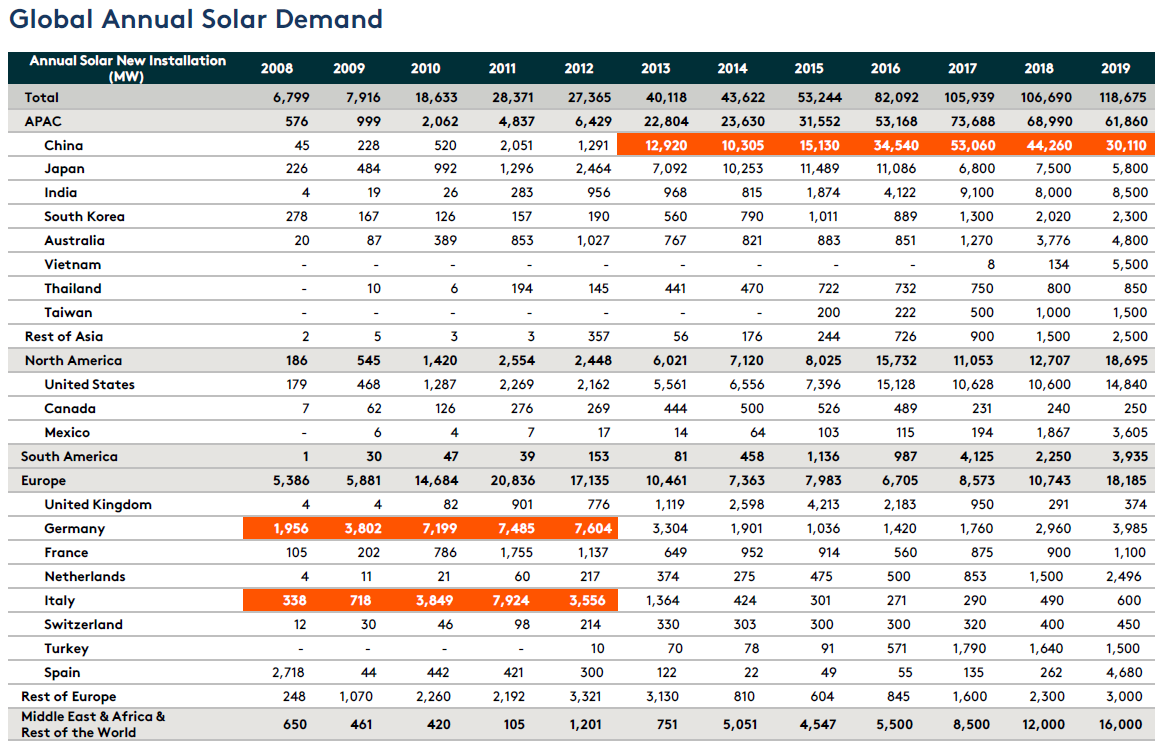

Wacker Chemie AG, a German company that was a producer of semiconductor-grade polysilicon, became the leading company in this field. Up until 2013, Germany and Italy were the key markets for photovoltaics. Since then, the Chinese government has instigated a push to take over global demand and supply.

The Time Horizon

When looking at the history of polysilicon, it would best to understand it in three phases:

- Phase I: Before 2008 -the leading supplier was Wacker Chemie AG, and key demand stemmed from Europe.

- Phase II: From 2008 to 2017 - demand switched from Europe to Asia. Asian leading companies, OCI and GCL, began working on mono and multi polysilicon cost cuts, respectively.

- Phase III: Post-2018 - downstream wafer leader Longi came out with mono products followed by new Chinese polysilicon makers producing at even lower costs.

Plan it, Source it, Make it

Wacker Chemie AG started the polysilicon business along the 16-kilometer Alz Canal that joins the Alz and Salzach rivers. The hydropower from the Alz River generates cheap and sustainable electricity even today, which has been one of Wacker Chemie AG’s key advantages. Energy cost accounts for 10% of Wacker’s total cost vs. industry level of over 30%1. Meanwhile, labor cost accounts for 34% vs. the industry level of 5%1. Wacker’s average annual labor cost was over 85,000 euros per capita in 2017, while that for a typical Chinese maker is only 10,000 euros1.

OCI and GCL started cost-cutting just from this point. The difference is that the two players were working on two different ways of cutting costs from $40/kg to $25/kg1. OCI focused on capacity expansion to enjoy the economies of scale and reduce fixed costs, such as factory construction D&A, some equipment sharing costs, and management fees. However, GCL was more focused on domestic substitution in equipment and technological improvement to ultimately cut machinery investment in addition to materials and energy consumption.

By 2010, GCL added more capacity, enjoyed extra benefits from economies of scale, and became a leader in cost minimization. However, GCL paid less attention to power costs at that time. They built the factory in East China, where power costs were as high as that in Korea and Germany. Post-2018, Longi replaced GCL as a new supply chain and technology leader. Other players such as Tongwei and Daqo learned from GCL’s mistakes and located new capacities in Southwest and Northwest China, where power costs were only one-third that of the East.

International politics and trade policies played an important role in industry dynamics. For example, China imposed anti-dumping and anti-subsidy tariffs on US polysilicon in 2012 as a response to US tariffs on Chinese solar cell exports. As a result, it made Wacker’s new factory in the US far less competitive than its counterpart Chinese players.

Faster, Better, Stronger

Polysilicon production is a typical chemical purification process with four key inputs: metallic silicon, purification equipment, energy, and labor. China is the biggest market exporting metallic silicon and enjoys the lowest retail power cost and labor cost. After domestic substitution of key equipment, Chinese players establish a competitive edge in mass production. As China becomes the biggest supplier, not only for polysilicon but wafer, cell, and module, the cost of logistics is lowered, and other concerns such as tariffs and supply chain stability being put at ease. Chinese players in the solar supply chain seem to be gaining market share against their overseas competitors.

The cash cost, average selling price, and liquidity are crucial factors for current players amid an economic downturn. In the long term, we believe that cost reduction is the key factor in driving companies to grow. The determinants for polysilicon are more so around efficient purification methods, cheaper equipment, and power, as well as automation. Should there be no exponential increase in the innovation of lowering power cost as well as any technological changes in methods, equipment, and automation, it would be a significant deterrent for new entrants.

It is easy to figure out the consolidation landscape following each player’s capacity expansion plan. Yet, if innovation takes place, either new entrants or existing players who have better technology adoption will be the winners. We should see a fresh start in industry dynamics rather than direct consolidation.

Our Foresight

From an investment perspective, we believe technology adoption is as important as technology innovation for players to thrive and expand. The industry players should have the right pipeline for new capacity adding in each medium term, demand timing, technology, location, a tradeoff between labor and automation, etc.

Production cost reduction is crucial for companies to burgeon. There are a few ways to cut costs: 1) Purification methods and equipment innovation to reduce energy consumption; 2) Economies of scale to lower fixed cost amortization; 3) Revolutionary changes to the silicon-based solar cell. Technological innovation and adoption could be the main drivers for the development of the industry.

Forward-looking in the near future, the top five Chinese polysilicon producers take a total market share of over 56%2. With the acceleration of the market consolidation, it is expected that the top five players will continue to hold the leading rank at the polysilicon market with its propelling demand, rapid urbanization, and demand for the product in end-use industries.

A Time to Reap the Opportunities

Mirae Asset believes the Chinese polysilicon market continues to dominate global production and consumption, with healthy growth in the foreseeable future. Our Global X China Clean Energy ETF allows you to enjoy the rising tide lifting in this industry.

THIS ARTICLE IS FOR EDUCATIONAL PURPOSES. NOT FOR SOLICITATION, OFFER OR RECOMMENDATION TO TRADE ANY SECURITIES.