Lithium, Explained

As the name suggests, lithium is an essential material used in lithium-ion batteries, which play an increasingly important role in areas like electric vehicles and renewable energy storage. The growth of these industries and their dependence on batteries is driving unprecedented demand for lithium, causing lithium miners and battery producers to rapidly scale operations. Despite the excitement around this natural resource, lithium contracts do not trade transparently on futures markets (like gold or oil), and therefore finding information and investing in the metal can be more nuanced than with other commodities.

The following analysis seeks to shed light on lithium by answering six questions:

- What is lithium and how is it used?

- What is driving lithium demand?

- What is the impact of the growth of battery megafactories in lithium?

- Where does lithium come from and how is it mined?

- What are the potential future prospects for lithium?

- How can one invest in lithium?

What is Lithium and How Is It Used?

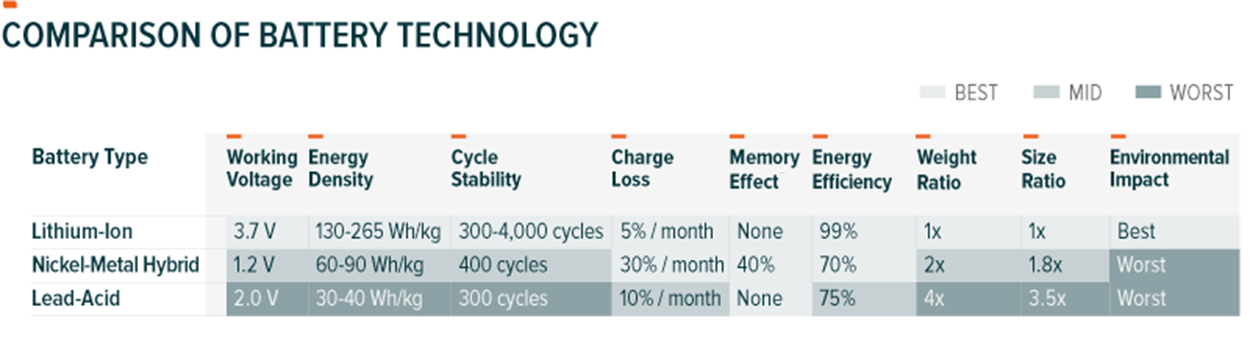

Lithium, the world’s lightest metal, has been dubbed “white petroleum” due to its color and common usage in state-of-the-art batteries powering a range of devices and vehicles. As demonstrated in the table below, lithium-ion is generally lighter, more efficient, and more durable than competing battery chemistries. This makes it a desirable choice for energy storage, particularly in vehicles and consumer electronics where weight and heavy usage are significant considerations. These applications can include electric and hybrid vehicles, scooters, smart phones, laptops, power tools and cameras, among other things.

(Note: Wh/kg = Watt-hour per kilogram)

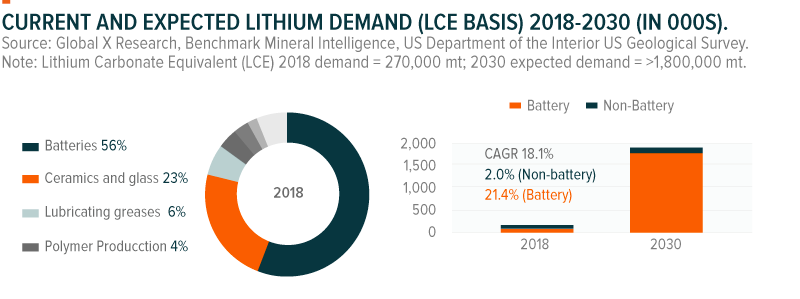

It is important to note that despite lithium’s common association with batteries, nearly half of current lithium demand comes from industrial applications, such as glass, ceramics, lubricants, and casting powders. However, much of the expected demand growth and optimism for lithium comes from the battery segment. Approximately 90% of lithium demand is expected to come from the battery segment by 2030.

(Note: mt = metric tons; CAGR = Compound Annual Growth Rate)

What is Driving Lithium Demand?

Within the battery segment, the most significant opportunity for lithium demand growth comes from electric vehicles (EVs). The average electric car uses over 5,000 times more lithium than a smartphone to power the vehicle’s range. Higher range electric cars with greater battery energy density, like the Tesla Model S, can use as much lithium as 10,000 smartphones.1 Therefore, growth of the electric car market will have a profound impact on total lithium demand.

In 2019, global car production of approximately 2 million EVs consumed approximately 137 thousand tons of lithium.2 But by 2030 this number could reach over 1.5 million tons of lithium as electric and hybrid cars become more prevalent as consumers consider clean energy, lower maintenance costs, and improved performance.3 Factoring in the expected incremental demand from renewable energy storage and consumer electronics, overall lithium demand growth could accelerate dramatically.

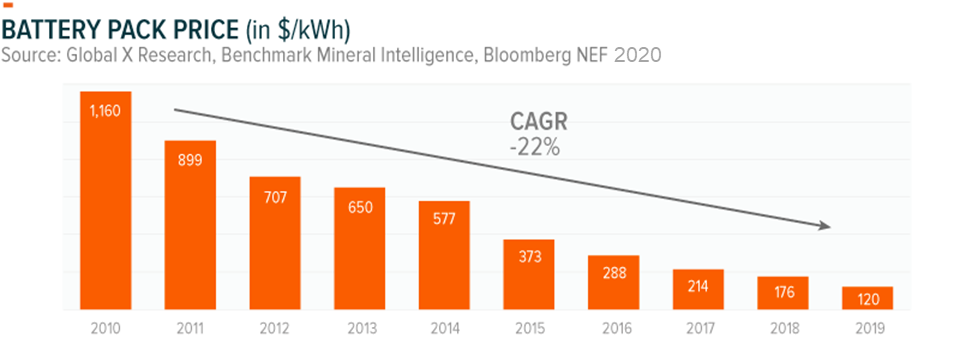

According to SignumBOX, lithium accounts for less than 3% of the total costs of a lithium-ion battery.4 Given its relatively small influence on a battery’s economics, overall lithium-ion battery prices could fall from gains in production efficiencies even if lithium prices increase. Battery manufacturers rely heavily on economies of scale to improve operational efficiency and enhance battery designs. Alongside increasing output, battery prices fell by an average of 22% annually over the last 10 years.5 Lithium-ion battery prices should continue this trajectory, causing EVs to become increasingly competitive with their internal combustion engine (ICE) counterparts, which in turn is likely to cause a surge in demand among mass market car buyers.

(Note: $/kWh = USD / Kilowatt-hour)

Where Does Lithium Come From and How Is It Mined?

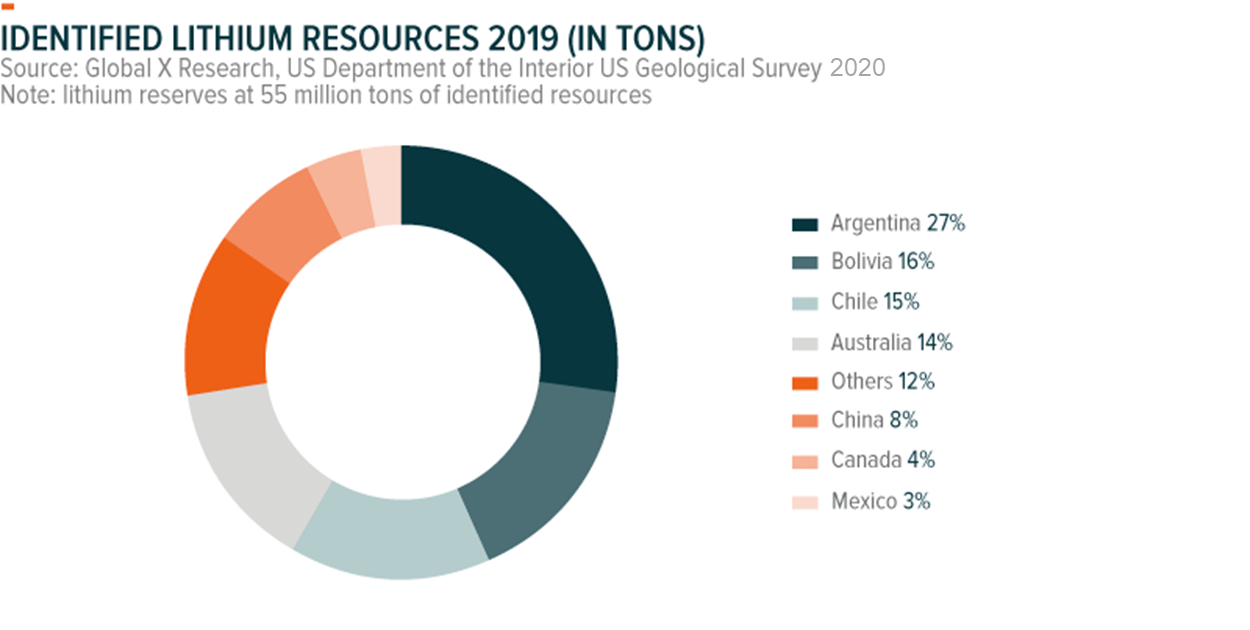

Lithium deposits are most prevalent in South America, particularly in Bolivia, Chile, and Argentina, which together are responsible for more than half of global lithium resources.6 Australia and China are two other countries with large lithium reserves, controlling approximately 14% and 8% of the world’s deposits, respectively.7 Currently, production in the lithium market operates under an oligopoly-like structure, with only a few companies controlling the vast majority of supply. However, new market participants have entered over the last few years, seeking to capture a piece of the rising demand.

Lithium comes from two main sources: brine and hard rock. Brine deposits are found in salt lakes where lithium is extracted through an evaporation process. Brine harvesting is historically a simpler, more common method of extraction, but generally yields lower grade lithium. Hard rock lithium mining, which is gaining relevance, requires geological surveys and drilling through rock, which can increase costs, but also often results in higher grades.8

Current hard rock projects require an average of 3-4 years of capital expenditures prior to production and an average mine life of 16 years. Brine projects require an average of 5 or more years of capital expenditures prior to production, but enjoy a longer life estimate of 30 years.

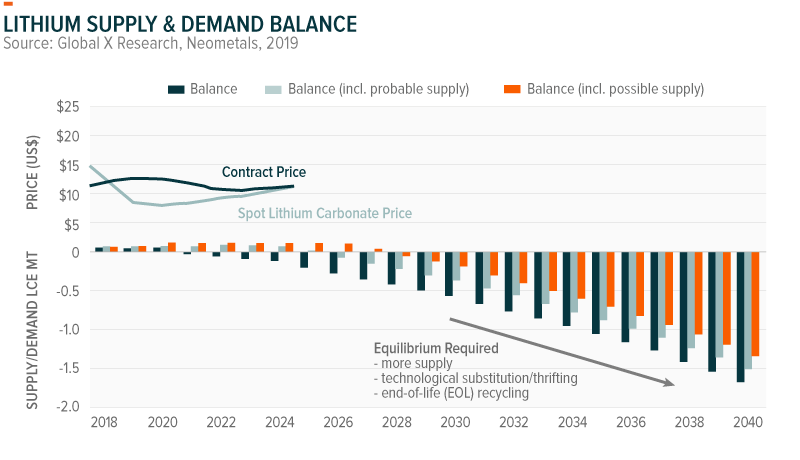

Based on production estimates by existing producers, there is expected to be a shortfall in the supply of lithium in the mid-2020s, as shown in the chart below. Historically, supply shortfalls in a commodity lead to upward pressure in the underlying resource’s price. Estimates place the world’s lithium reserves at 55 million tons of identified resources but given the time it takes to bring a new project to market, supply and demand forces could push medium-term lithium prices higher.9

What Is the Impact of the Growth of Battery Megafactories in Lithium?

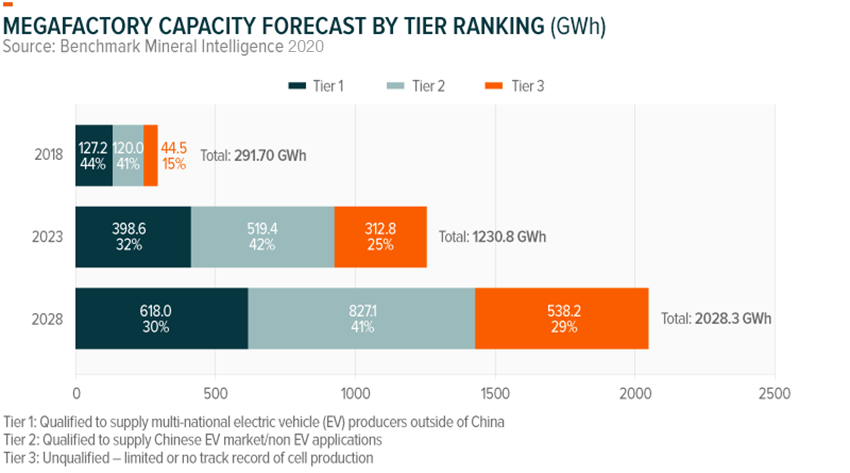

The term ‘megafactory’ has become a battery industry buzzword to describe enormous lithium-ion production plants, that turn raw materials into finished batteries and typically have an annual output greater than 1 GWh (Gigawatt hours). For context, 1 GWh is equal to the battery capacity required to supply approximately 20,000 Tesla vehicles.

With Tesla’s announcement of their 4th battery megafactory, the total number of battery megafactories around the world should reach 115.10 Combined, these megafactories are expected to produce over 2,000 GWh annually by 2028, almost 7 times current capacity levels, representing enough capacity to manufacture 40 million EVs.11 At this planned capacity, the industry would require at least 1.6 million metric tons of lithium each year, raising the question of whether the lithium industry will be able to meet expected demand.12

Effective battery production has proven to require expertise, consistent access to key raw materials, and scale. Therefore, auto manufacturers around the world typically rely on third party battery manufacturers rather than making the batteries in-house. There are a few exceptions though. Companies like Tesla, jointly with Panasonic, designed and engineered their own batteries. BYD, the Chinese automaker, is another example of an EV company that builds its own batteries.

What are the Potential Future Prospects for Lithium?

There are three important trends that could continue to provide support for lithium and battery demand growth over the coming years:

- Electric vehicles powered by lithium batteries continue to see scaling production levels and capital investments. By 2040, electric vehicles are expected to reach over 50% of all new vehicle sales, surpassing internal combustion engine (ICE) vehicles, as costs for lithium-ion batteries decrease and technology improves.13

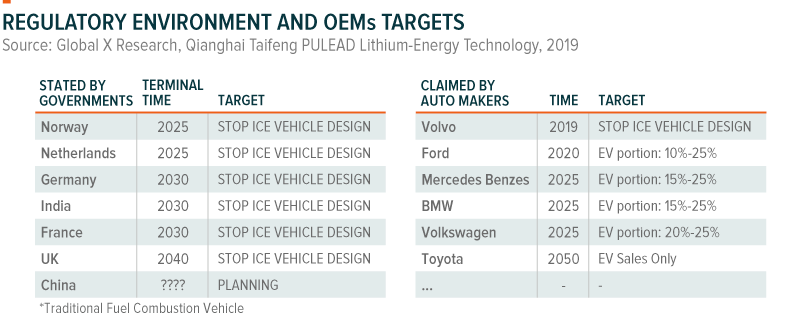

- Governments worldwide continue to support the adoption of EVs, establishing regulations to phase out the production and sale of ICE vehicles over the coming decades.

- Electric grids continue to utilize lithium batteries as a method of energy storage, particularly for renewable sources like solar and wind.

(Note: OEM = Original Equipment Manufacturer)

Conclusion

Lithium demand is expected to rapidly increase as batteries play an increasingly critical role in electric transportation, renewable energy storage, and mobile consumer electronics. As the world electrifies, lithium miners and battery producers present a compelling investment case as companies well-positioned to benefit from this disruptive trend.